Montana First-Time Home Buyer Programs and Grants of 2022

Key Takeaways:

- First-time home buyers in Montana can access 30-year fixed-rate loans at below-market interest rates via the Regular Bond Loan program.

- Down payment assistance is available in the form of a long-term loan that may not require monthly payments, depending on which program you qualify for.

- Tax benefits up to $2,000 per year are available to first-time homeowners via the Mortgage Credit Certificate (MCC) program.

If you’re thinking about becoming a homeowner in Montana, take a few minutes to check out the many programs and grants available to first-time buyers. These programs can help you access below-market interest rates on your loans, down payment and closing cost assistance, and even reduce how much you pay in taxes at the end of the year!

The only catch is that you’ll have to meet the eligibility requirements. Some of these programs are fairly complex, so it’s worth your time to understand what they offer and what their eligibility requirements are. Let’s explore.

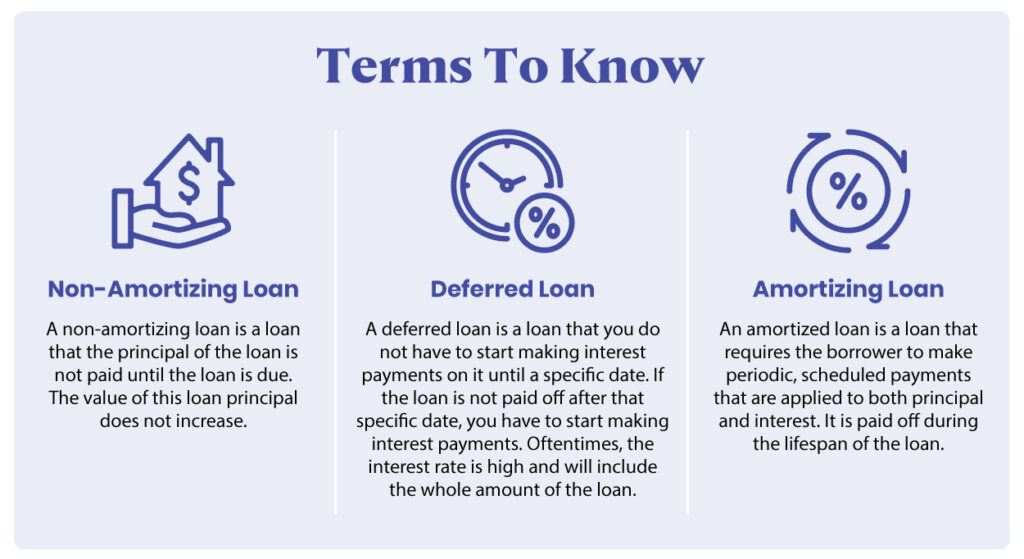

Mortgage Terms To Know

- Deferred Loan – A deferred loan is a loan that you do not have to start making interest payments on it until a specific date. If the loan is not paid off after that specific date, you have to start making interest payments. Oftentimes, the interest rate is high and will include the whole amount of the loan.

- Non-Amortizing Loan – A non-amortizing loan is a loan that the principal of the loan is not paid until the loan is due. The value of this loan principal does not increase.

- Amortizing Loan – An amortized loan is a loan that requires the borrower to make periodic, scheduled payments that are applied to both principal and interest. It is paid off during the lifespan of the loan.

Montana Housing Regular Bond Program

The Montana Housing agency has a number of programs that are open to first-time buyers – but the Regular Bond Loan program was specifically created with first-time buyers in mind. This program offers 30-year, fixed-rate loans at below-market interest rates for qualified Montana first-time home buyers, so long as you meet the requirements.

Regular Bond Program Eligibility Requirements

To be eligible for the Regular Bond Program, you must:

- Qualify for the underlying loan package through a participating lender. These packages include FHA, VA, RD, and HUD-184 loans.

- Be a first-time home buyer, defined as anyone who has not owned a principal interest in a home within the last three years.

- Meet income and purchase price limits (more on that shortly)

- Use the purchased home as your primary residence. If a business is conducted in the residence, the space that business occupies cannot exceed 15% of the total area of the home.

- Funds through the program cannot be used to refinance an existing loan.

- Loans may be used to purchase single-family homes, condos, and manufactured homes. Manufactured homes must have been built after 1976 and permanently affixed to the foundation. The property acreage for any purchase cannot exceed 40 acres, per the Montana Small Tract Financing Act.

- All borrowers must complete a Montana Housing approved home buyer education program.

Income and Purchase Price Limits

All loans processed through Montana’s Regular Bond Program require applicants to meet the income and purchase price limits set by Montana Housing. These limits ensure that the program remains available for individuals with lower household incomes.

To learn more, view the current list of income and purchase price limits along with the current interest rates for the various Montana Housing loan programs.

Down Payment Assistance Programs

Of course, coming up with the liquid cash necessary to buy a home can be tricky. To make homeownership more affordable, Montana Housing offers financial assistance programs. Though these programs are billed as down payment assistance, the funds you secure through the program can be used towards your closing costs as well!

Here are the major highlights of each program:

Bond Advantage Down Payment Assistance Program

The Bond Advantage program gives any eligible Montana first time home buyer up to 5% of the sale price of the home, up to a maximum of $10,000. This money comes in the form of a 15-year amortizing loan with low monthly payments. In order to access those funds, you’ll need to meet the following eligibility requirements:

- You have a 30-year first mortgage through a Montana Housing program.

- Your credit score is 620 or higher.

- You must complete an approved education program.

- Your minimum contribution to the transaction is $1,000.

MBOH Plus 0% Deferred Down Payment Assistance Program

The MBOH Plus 0% Deferred Down Payment Assistance Program offers a more favorable loan structure than the Bond Advantage program but has much more strict eligibility requirements.

The MBOH Plus assistance comes in the form of a loan for up to 5% of the purchase price of the home, up to a maximum of $6,500. However, unlike the Bond Advantage program, the MBOH Plus loan is a 0% interest, non-amortizing loan. Non-amortizing means that you won’t have to make monthly payments on the loan unless you sell or transfer the title of your property, or you pay off your first loan. This makes it a great deferred payment option for those who qualify.

Here are the basic eligibility requirements of the MBOH program:

- Borrowers must have a 30-year first mortgage through a Montana Housing loan program.

- Borrowers must have less than $55,000 annual income.

- A credit score of 620 is required, and all borrowers must have less than a 43% debt-to-income ratio. This is calculated by dividing your total recurring monthly debts by your monthly gross income.

- All borrowers must contribute at least $1,000 to the transaction and complete an approved home buyer education program.

NeighborWorks Montana Down Payment Assistance

NeighborWorks Montana (NWMT) offers a number of down payment assistance products that might help the first time home buyer who doesn’t qualify for financial assistance through Montana Housing.

NWMT assistance packages are second-mortgage loans that can be either amortizing or deferred. All three of these programs require borrowers to complete an approved home buyer education course. Here are the options:

The 20+ Community Second offers an amortizing second loan for buyers with an income of 120% or less of the Area Median Income (AMI). The Community Second requires a minimum loan amount of $10,000, and you’ll be required to make monthly payments on it. This loan can be used to place a high enough down payment on your first mortgage so that you eliminate the need for private mortgage insurance (PMI).

The State HOME Deferred is a non-amortizing, 0% deferred loan for first-time home buyers in eligible areas across the state who make 80% or less of the AMI. Up to $40,000 can be borrowed under this program. No monthly payments are due until 15 years have passed (extends to 30 years if the borrower remains in the home), or if the home is sold, rented, or the first mortgage is paid off.

NWMT’s Statewide Low-Mod program offers an amortizing second mortgage of up to $10,000 for individuals who make below 125% of the HUD median income for that area when adjusted for family size. For FHA mortgages, the threshold is 115% of the HUD median income. The loan terms are 15 years for families over 80% of the HUD median income. It also can go up to 30 years for borrowers with less than 80% of the HUD median income. Interest rates vary depending on the borrower’s first loan lender, and their income when compared to the HUD median income in the area.

Mortgage Credit Certificate (MCC)

Montana Housing also offers a Mortgage Credit Certificate (MCC) program, which gives first-time buyers in Montana a tax break to make home ownership more affordable. An MCC is simply a credit given to first-time buyers that allows them to apply up to 20% of the mortgage interest they’ve paid throughout the year to their tax liability, up to $2,000.

For example, let’s say that you’ve paid $10,000 in mortgage interest throughout the year. 20% of that amount would be $2,000 (the maximum amount allowed under the program). That $2,000 is then applied to any tax liability you might have at the end of the year. So if you owed $3,000 in taxes, you now only owe $1,000. As an added advantage, the remaining 80% of your mortgage interest can be included as an itemized deduction.

Here are a few key details about Montana’s MCC program:

- It’s good for the lifetime of the loan, provided you stay in your home.

- You must meet income limits to qualify; income limits vary based on the size and location of your household, and range from $70,500 to $121,800.

- You must be a first-time home buyer, with exceptions for some veterans or housing purchases in “Targeted areas.”

- The purchase price of the home must not exceed a certain limit. That limit falls somewhere between $283,348 and $454,142 depending on where the home is located in Montana.

- You’ll have to pay a one-time fee at closing to secure the MCC.

Closing Thoughts

If you meet the eligibility requirements, Montana’s programs for first-time home buyers can be a great option! These programs give eligible buyers access to below-market interest rate loans, as well as optional down payment assistance in the form of a second mortgage which may not require a monthly payment (depending on the program).

For those first-time buyers who don’t qualify for a Montana Housing loan program, there are still some programs that can help you with your down payment or reduce the amount of money you’re paying in interest. NeighborWorks Montana offers three down payment assistance programs, some of which don’t require a monthly payment and accrue no interest. Additionally, Montana Housing can issue a Mortgage Credit Certificate on any loan statewide, provided you meet the requirements of the program.

If you aren’t sure which option is right for you, consider completing a home buyer education course. Home buyer education can demystify the home buying process, reduce anxiety, and help you find the right home for your budget. Want to learn more about a specific loan program? Just contact a Montana Housing Loan Program Participating Lender.